43. How SMBs in Finance Can Leverage AI APIs for Fraud Detection, Automation, Personalized Banking, and Risk Analysis

In this article, we’ll explore how SMBs in finance can harness AI APIs to supercharge their operations. We’ll focus on key applications – fraud detection, process automation, personalized banking, AI-driven chatbots, and risk analysis – and highlight the top AI API providers enabling these solutions (including OpenAI, AWS, Microsoft Azure, Google Cloud, IBM Watson, and fintech-specific platforms). We’ll also discuss best practices for seamless integration and dive into examples of industry players who successfully rode this wave. The goal is to provide a strategic roadmap for decision-makers (CFOs, CTOs, CIOs, etc.) to innovate with AI while keeping practicality and ROI in focus.

Q1: FOUNDATIONS OF AI IN SME MANAGEMENT - CHAPTER 2 (DAYS 32–59): DATA & TECH READINESS

Gary Stoyanov PhD

2/12/202527 min read

1. Why AI API Integration is a Game-Changer for SMB Finance

For small and medium financial institutions, staying competitive is tough. Margins are thin, compliance costs are high, and customer expectations in the digital age keep rising. AI can be a game-changer on multiple fronts:

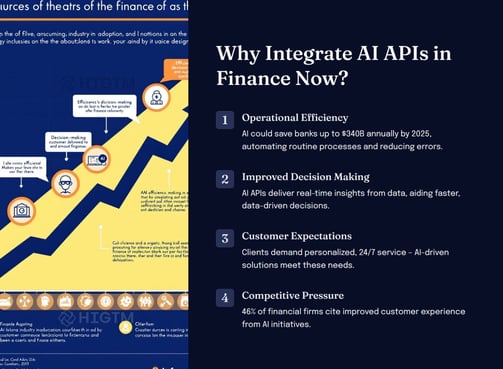

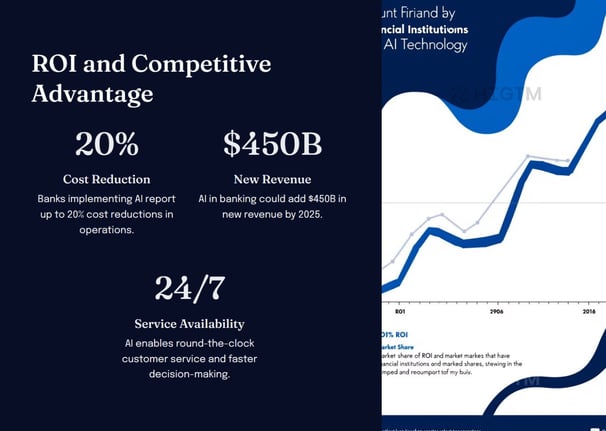

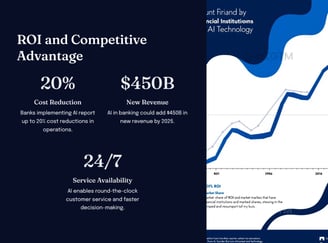

Cost Efficiency and Scale: AI automation can handle tasks at scale without proportional increases in cost. For example, an AI service can review thousands of transactions for fraud in seconds, a job that would require an army of analysts. This drives down operating costs – studies suggest AI could reduce operational expenses in finance by up to 22-25% on average. It also means an SMB can scale up services (like monitoring more accounts or processing more loans) without a linear increase in headcount or manual effort.

Improved Accuracy and Risk Management: AI systems excel at detecting patterns and anomalies. In finance, this translates to catching fraudulent transactions that humans might miss, or identifying subtle indicators of credit risk earlier. A traditional rule-based system might flag 1,000 potential frauds that staff must investigate (with many false alarms), whereas an AI might narrow it down to the 50 truly suspicious cases – saving time and preventing losses. In fact, AI-based fraud detection has helped institutions cut fraud-related losses significantly, sometimes by double-digit percentages, by reacting faster than old-school methods.

Enhanced Customer Experience: Today’s customers expect personalized, instant service – whether it’s a prompt answer from their banking app or a loan offer tailored to their situation. AI APIs enable this by powering chatbots, virtual assistants, and recommendation engines. These tools can handle customer queries 24/7 and analyze customer data to personalize offerings. According to a recent industry survey, improved customer experience was the top value driver of AI in financial services (noted by 46% of respondents). SMBs, often known for personal touch, can amplify that strength with AI – providing “mass personalization” that feels bespoke for each client.

Data-Driven Insights and Decision Speed: Finance runs on data, and most SMBs are sitting on a trove of information (transactions, customer profiles, market data) that could inform better decisions. AI APIs (like those for machine learning or analytics) can crunch these datasets to surface trends or predictions that would be impossible to derive manually. For instance, an AI might analyze transaction histories to predict which customers are likely to churn or which loan applicants might become delinquent, allowing the business to take proactive action. Faster, AI-assisted analysis also means quicker decision cycles – what took weeks can sometimes be done in minutes – giving smaller firms agility in responding to market changes.

Lower Barrier to Entry through APIs: Historically, adopting AI meant hiring data scientists and building models in-house – something out of reach for many SMBs. APIs (Application Programming Interfaces) changed the game. They allow companies to consume AI as a service. Via API, an SMB can send data to, say, an image recognition service to process a check image, or to a language model to generate a financial summary, and get results instantly. No need to develop the complex AI model yourself – the heavy lifting is done by the provider. This “AI-as-a-service” model dramatically lowers the barrier to entry, making advanced capabilities accessible on a pay-as-you-go basis.

In short, integrating AI through APIs empowers smaller financial players to innovate rapidly without massive upfront investments. It’s a way to leapfrog, offering sophisticated features and efficiency on par with (or even beyond) larger competitors. As we move forward, we’ll delve into specific areas where this strategy is making waves.

2. Key AI API Applications in Finance

Let’s break down the top areas in finance where AI APIs are being applied successfully, and how SMBs can leverage them:

2.1 Fraud Detection and Financial Crime Prevention

Fraud and cybercrime are ever-present threats in finance. Traditional fraud rules (e.g., flag transactions over $X or from foreign locales) catch some cases but are too simplistic and generate many false positives. AI-driven fraud detection uses machine learning algorithms that continuously learn from transaction patterns. They can detect unusual behaviors – maybe a subtle change in a customer’s spending pattern or a combination of factors that hint at fraud – which rules would miss.

How APIs help: Major cloud providers offer fraud detection as a service. For example, Amazon Fraud Detector (AWS) allows you to input transaction data via API and returns a fraud risk score. It’s built on machine learning models trained on large datasets of fraudulent and legitimate transactions. Similarly, providers like Featurespace (with their ARIC platform) focus on fraud/AML; banks send event data through APIs and receive real-time alerts if something looks fishy. An SMB can integrate these APIs into payment systems or core banking platforms. When a customer swipes their card or initiates a transfer, the system calls the fraud API, and if the score is high-risk, it can automatically pause the transaction or route it for manual review.

Case in point: Stripe Radar (integrated into Stripe’s payment API) uses AI to detect fraudulent charges for online businesses. SMBs using Stripe automatically benefit from this without any development on their part – the API scores each transaction for risk, helping merchants avoid chargebacks. For an in-house example, a regional bank might use AWS’s fraud detection API on their credit card transactions; over time, they notice a reduction in fraud losses and also fewer false alarms, which means their fraud team can focus on true threats.

Best practices: When implementing AI fraud detection, feed the API as much relevant data as possible (transaction amount, location, merchant, customer history, etc.). The more context, the better the AI can decide. Ensure a feedback loop – if a transaction was flagged and later confirmed (fraud or legit), send that info back to train the model (some services allow this). Also, be mindful of latency: these checks need to happen fast. Most AI APIs are optimized for speed, but you should test and be ready with fallback rules if an API is temporarily slow or unavailable.

2.2 Automation of Financial Processes

Many finance processes are repetitive and rule-based: processing invoices, reconciling accounts, generating quarterly reports, updating compliance checklists, etc. AI can automate a lot of this grunt work. Two sub-areas stand out: Intelligent Document Processing and Report Generation/Analysis.

Intelligent Document Processing: AI services can now extract and interpret data from documents like invoices, receipts, bank statements, or loan applications. For instance, Google Cloud’s Vision API and Document AI can parse PDFs and images to pull out structured data (e.g., vendor name, invoice number, amounts due). Microsoft’s Azure Form Recognizer does similarly. Through an API, you can send a document and get back key fields in JSON. An SMB can use this to automatically feed invoice data into their accounting system, or to scan loan documents during underwriting without manual data entry. This reduces errors and speeds up workflows dramatically.

Report Generation and Analysis: Natural Language Generation (NLG) APIs can draft narratives from data. Imagine closing the books and having an AI service produce a first draft of your financial commentary (“Revenue increased 5% QoQ due to growth in the retail segment, while expenses...”). OpenAI’s GPT-4 or other language model APIs can be used for this – you pass in the raw numbers or bullet points, and the AI produces a human-like summary. Similarly, AI can analyze data and highlight trends or anomalies. For example, IBM Watson Studio or Azure AI can be set up to analyze large datasets (via API or pipeline) and output insights (like “Branch X had an unusually high cash withdrawal volume this week”).

SMB advantage: By automating these tasks, small teams can do more with less. A mid-sized bank might automate its compliance reports by having an AI cross-check transactions against regulatory rules and fill out report fields. Or a fintech startup might use AI to handle customer onboarding paperwork – verifying IDs and extracting info – thus scaling up customers without needing a big ops team.

Real example: Ocrolus is a fintech that offers an API for document analysis, heavily used in loan processing. Lenders (including SMB banks and online lenders) feed bank statements or pay stubs into Ocrolus’s API, which uses AI to transcribe and analyze them for key metrics (average balance, income trends). This helped many lenders speed up loan underwriting and even enable fully digital loan applications. Another example is using an RPA (Robotic Process Automation) tool with AI capabilities: some SMB finance departments use platforms like UiPath or Automation Anywhere (which increasingly embed AI for tasks like reading PDFs) to automate workflows end-to-end.

Best practices: For document AI, test the API on your specific forms – accuracy can vary if your documents have unusual formats, so sometimes a bit of training or template tweaking is needed. Always have a manual review process for critical data at the beginning to verify the AI’s output until confidence is built. For NLG (report writing) and analysis, ensure sensitive data is handled properly – if using a cloud API, check where the data is stored. Some companies opt for on-prem versions of these AI models for confidentiality (OpenAI, for instance, allows dedicated instances for enterprises). And remember, automation should augment your staff, not alienate them – involve your team in designing the workflow so they trust and understand the AI (e.g., your accountants should know how the AI-generated report is created and be able to edit its output).

2.3 Personalized Banking and Customer Experience

Personalization in banking can mean the difference between a one-time customer and a lifetime customer. AI helps by analyzing customer data (transactions, demographics, preferences) to tailor services and communications.

Recommendation Engines: Similar to how Netflix suggests movies, AI can suggest financial products. For example, if a small business customer’s account shows growing cash balances, the system might prompt a line-of-credit offer or a treasury management service. AI models (like those available via Amazon Personalize or open-source frameworks) can be integrated to deliver these recommendations through your CRM or marketing system. Via API, you could send customer behavior data and receive product recommendations ranked by relevance.

Customer Segmentation & Marketing: AI APIs can cluster customers into segments far more nuanced than traditional methods. Instead of segmenting by just age or income, an AI might find “customers who use mobile app daily and have moderate account balances but no investment accounts” – an actionable micro-segment to target with a new offering. Cloud providers offer machine learning APIs or AutoML services that can be fed customer data to find patterns. Google’s AI Platform (Vertex AI), for instance, could be utilized to train a model on customer churn or product propensity and then served via API for real-time use.

Dynamic Personalization in Apps: If you have a digital banking app or a fintech product, AI can personalize the in-app experience. For instance, an AI API could determine what news articles or tips to show each user (e.g., an investor gets stock market news, a new saver gets budget tips). This is done by analyzing user behavior and preferences with AI – something even a modest development team can implement by calling a personalization API and having the app adjust content accordingly.

Example: Wells Fargo’s AI-driven personalized insights – Wells Fargo (a large bank, but the approach is instructive) integrated an AI that analyzes customer accounts to generate personalized “insights”, such as notifying someone: “Looks like you’ve been paying $X in ATM fees this month – consider using our partner ATMs for free.” While they likely built it in-house, today an SMB could approximate this by using an API to analyze transaction data for patterns and then crafting rules or messages based on the output.

Another example at a smaller scale: a credit union could use Cognitive APIs from Azure to analyze call center transcripts and figure out what each customer is concerned about (maybe many are asking about mortgage refinancing). That insight can feed into personalized email outreach – e.g., send those interested in refinancing a tailored offer. This kind of text analysis and sentiment detection is available via APIs (Azure Text Analytics, Google Cloud Natural Language, IBM Watson NLU, etc. all provide sentiment and key phrase extraction from text).

Best practices: Beware of the “creepy factor.” Just because AI finds a pattern doesn’t mean you should always act on it overtly. Ensure that personalized offers or messages feel helpful, not intrusive. Also, maintain privacy – personalization should work within the bounds of consent given by customers for data use. In terms of integration, start simple: one or two personalized elements (like a recommended product on the dashboard) rather than a complete overhaul. Measure engagement – do customers click the AI-driven suggestions? Use that to refine the algorithms. Over time, as trust in the AI grows, you can expand its role in customer interactions.

2.4 AI-Driven Chatbots and Virtual Assistants

Chatbots have become a staple in customer service, and AI APIs make them smarter and more human-like. In finance, AI chatbots can handle balance inquiries, FAQs, simple transactions (like transfers), and even more complex tasks like guiding a customer through a loan application pre-screening.

Natural Language Processing (NLP) APIs: The likes of OpenAI (ChatGPT API), IBM Watson Assistant, Google Dialogflow, and Microsoft Bot Framework with LUIS allow you to add conversational AI capabilities without developing NLP from scratch. For instance, IBM Watson Assistant comes pre-trained on common intents (especially in banking, since IBM has many financial clients) and you can customize it via a visual interface, then deploy via API to your channels (website chat, mobile app, even WhatsApp). OpenAI’s GPT-4 can be used to interpret and generate text with a high degree of fluency – some banks are experimenting with it to allow customers to ask complex questions (“Can you summarize my spending habit this month?”) and get a coherent answer.

24/7 Customer Support and Beyond: An SMB can deploy a chatbot to answer, say, 100 common customer questions. This reduces call center volume. Importantly for finance, modern chatbots can authenticate users and perform tasks securely. For example, a chatbot might help a user reset their card PIN or report a lost card (after verifying identity with an OTP code). Some trading fintech apps have chatbots that even execute trades for you when you type “Buy 10 shares of X”.

Internal Assistants: The power of AI chatbots isn’t just external. Internal teams can use them too. Imagine a finance team member asks a bot, “Pull up the Q1 expense report” or “What’s the latest cash position of Client Y?” – the bot, integrated with internal databases via API, can fetch that instantly. This is essentially a friendly front-end to your data. Companies are using tools like Azure’s QnA Maker (now part of Cognitive Services) to create internal knowledge bots. As a small organization, you can similarly deploy an internal FAQ bot for employees (covering HR, IT, or in-house analytics) relatively easily.

Success story: Bank of America’s Erica is one of the famous examples – a virtual assistant in their mobile app that uses AI to handle over a billion interactions, from simple queries to more advisory prompts (Erica might say, “I see you spent more on restaurants this month, need help budgeting?”). For smaller players, solutions like Kasisto’s KAI (a fintech-focused conversational AI platform) offer pre-built banking AI brains that can be integrated via API into a mobile app or website. This allowed even community banks to launch sophisticated chatbots without years of development.

Best practices: Aim for a hybrid approach – chatbots for common tasks, with easy escalation to a human for complex issues. Always let the user know they’re talking to an AI (transparency builds trust). Security is paramount: ensure the API integrates with your authentication systems so that private info is only given out after verifying the user. Train the bot iteratively – start with a narrow scope (maybe just FAQs about hours and locations, or basic account info) and then expand as it learns from interactions. Leverage existing libraries of intents (no need to reinvent “What’s my balance?” – many chatbot platforms have this out-of-the-box for banking). Finally, track metrics: containment rate (how many inquiries the bot handles without human help), customer satisfaction scores, etc., to continuously improve.

2.5 Risk Analysis and Decision Support

Risk management is core to finance – whether it’s credit risk, market risk, or operational risk. AI is enabling more predictive and granular risk analysis.

Credit Scoring and Underwriting: Traditional credit scoring looks at a handful of variables. AI models, on the other hand, can analyze thousands of data points (including alternative data like rent payments, education, even how you fill out a form) to assess creditworthiness. Startups like Upstart have built AI models for lending that outperform traditional FICO-based models, allowing lenders to approve more good borrowers that were previously overlooked. They offer this via API to banks – basically, a bank sends applicant data and the API returns a “approve/decline and interest rate” recommendation. For SMB lenders, this is transformative: you can instantly add a sophisticated AI brain to your underwriting without developing it. Similarly, companies like Zest AI or FICO with its AI offerings provide API solutions to augment credit decisions.

Market and Investment Insights: For firms dealing in investments or needing economic forecasts (even a local bank managing its investment portfolio), AI can churn through market data and news to provide insights. Kensho (owned by S&P Global) is known for its AI analytics on financial markets – for example, via API it can answer questions like “What happens to airline stocks when oil prices go up 10%?” by analyzing historical data. While this is more niche, the rise of AI in investment research means there are APIs that can, say, summarize SEC filings (IBM Watson used to offer this service) or detect sentiment from news that could affect your asset valuations.

Operational Risk & Compliance Analytics: AI can also predict operational issues – e.g., which processes are likely to fail or which transactions might violate compliance. Some banks use AI to analyze communication (emails, chat) to flag compliance risks or even employee fraud. Natural Language Processing APIs (like those from Google or AWS Comprehend) can scan text for certain themes or anomalies. For example, an AI could flag if an employee email contains phrases that suggest unethical behavior (a bit “Big Brother”, but some financial firms do this to preempt scandals).

Real-world usage: Morgan Stanley’s “Next Best Action” for advisors is an AI that looks at client portfolios and market conditions, then suggests tailored actions for each client (like rebalancing or proposing a different investment). This kind of recommender system for risk/portfolio management is essentially an AI integration – combining data from internal systems and analytics from AI models. On the credit side, as mentioned, multiple community banks now use Upstart’s API or similar to approve loans faster and with confidence, often resulting in higher approval rates and lower defaults.

And for compliance, HSBC reportedly has used AI to monitor transactions for money laundering with greater accuracy, by integrating AI from a firm called Ayasdi. Mastercard uses AI (Brighterion) in its network to score every transaction’s fraud risk in real time – an example of risk management at scale via an integrated AI (Mastercard’s system connects to banks and merchants via APIs sending back risk decisions in milliseconds).

Best practices: In credit and risk, explainability is key. If you use an AI API to help make lending decisions, you need to ensure you (and regulators) can understand why it’s deciding that. Some APIs provide reason codes or at least key factors. Always test the AI on historical data before trusting it fully – see if it aligns with your domain expertise and doesn’t exhibit biases (e.g., unintentionally disadvantaging a protected group – if it does, retrain or adjust factors). Also, treat AI outputs as decision support, especially initially, not absolute truth. Let your risk officers and analysts review the AI recommendations and over time as trust builds, you can automate more. Finally, continuously update the models – economic conditions change (as we saw in the pandemic) and risk models need to be recalibrated. Many AI API providers will handle model updates for you (ensuring they are using the latest data), but you’ll want to stay in tune with any drift or changes in performance on your data.

3. Who Are the Top AI API Providers for Finance?

We’ve mentioned many providers in passing. Here we’ll summarize the key AI API players SMBs should consider, and their relevance to financial applications:

OpenAI: Renowned for its GPT-3.5 and GPT-4 models, OpenAI offers APIs that excel at natural language understanding and generation. For finance, this means superb capabilities in analyzing text (news, reports, customer messages) and generating human-like language (chatbot responses, report drafts). SMB use case: integrate OpenAI to power a customer support chatbot or to auto-generate personalized financial advice snippets for clients. OpenAI’s models can also assist in writing code or formulas – possibly useful if you want to automate some internal scripting or Excel analysis tasks. Notable: Morgan Stanley’s collaboration with OpenAI for advisor support shows the potential. Keep an eye on cost and data privacy – OpenAI API usage is charged per token, and you’d need to ensure no sensitive data is shared in a way that violates client privacy (OpenAI allows opting out of data retention by default now for business users).

Amazon Web Services (AWS): AWS has a broad range of AI services accessible via API. For finance specifically:

Amazon Fraud Detector: pre-built models for transaction and account fraud (great for payments and account opening fraud).

Amazon Comprehend: NLP for entity extraction, sentiment (could be used to analyze customer feedback or news articles).

Amazon Textract: OCR and form extraction (for document processing like reading pay stubs, IDs).

Amazon Lex: service for building chatbots (the same tech that powers Alexa’s voice understanding, tailored for text/voice chatbots).

Amazon Forecast: time-series forecasting which could aid in financial forecasting (cash flow, demand planning).

SageMaker: a platform to build and deploy custom models – if you have some data science resources to customize AI for your exact needs. AWS is often favored by institutions that already use AWS cloud; it’s scalable and known for security. For SMBs, AWS offers free tiers or low-cost tiers that let you experiment. Many fintechs (like Capital One, Monzo, etc.) have utilized AWS for their AI pipelines. Additionally, AWS has specific financial services competency partners – meaning if you need help, there are integrators who know both AWS and finance.

Microsoft Azure: Azure’s AI offerings are similarly rich:

Azure Cognitive Services: a collection of APIs for language (e.g. text analytics for key phrases, sentiment, language detection), vision (image recognition, OCR via Computer Vision and Form Recognizer), speech (speech-to-text and vice versa, which could be used for voice assistants or transcribing calls), and decision (anomaly detector, content moderator).

Azure OpenAI Service: Microsoft has partnered with OpenAI to offer GPT-4 and other models on Azure with enterprise-grade security. This is a big plus for finance companies concerned about data privacy – your data stays in your Azure instance.

Azure Bot Service: integrates with Cognitive Services (LUIS language understanding) to let you build chatbots and deploy them across channels easily. Azure is a strong choice if you’re a Microsoft-stack shop (using .NET, Azure cloud, etc.). They also have an edge in enterprise sales and support – helpful for SMBs that want more guided help. They are powering AI for many banks (for example, the Malaysian bank RHB launched an AI chatbot on Azure; UBS uses Azure for risk modeling, etc.). With Azure, you also get Power Platform AI integrations (Power BI has AI visuals, Power Automate can use AI builder – which is essentially simplified Cognitive Services for citizen developers).

Google Cloud: Google’s AI prowess is well-known. Offerings of note:

Dialogflow CX: a leading conversational AI platform (now part of Google Cloud’s Contact Center AI) – great for sophisticated chatbots/voicebots with multi-turn conversations (several banks and credit unions have built virtual assistants with Dialogflow).

Cloud Vision and Document AI: for image and document processing – very useful for automating ID verification, invoice processing, etc., as discussed.

Cloud Natural Language API: for text analysis (entities, sentiment, classification).

AutoML Tables/Vertex AI: Google’s tools to train custom models on your data with minimal coding. For example, you could train a custom model to predict loan default using Vertex AI, then serve it via API endpoint.

BigQuery ML & AI: If you’re already using Google’s BigQuery for data warehousing, you can do ML directly in SQL or call AI models from there; not an external API per se, but worth mentioning if your data lives in GCP. Google’s cloud is also strong in data analytics (BigQuery, Data Studio) which often complements AI projects. Many fintech startups (like LendingClub, etc.) have utilized GCP for its data and AI capabilities. One of Google’s advantages is its research leadership (they often have very advanced models, though sometimes they appear in Google’s own services before being externalized).

IBM Watson (IBM Cloud): IBM has tailored many of its AI offerings to industries like finance:

Watson Assistant: a top-tier conversational AI platform. IBM has case studies of banks using it for customer service and even voice assistants in call centers.

Watson Discovery: an AI search and text analysis tool – useful for digging insights out of large document repositories (think of scanning through all your loan contracts to find certain clauses or risks).

Watson OpenScale & Explainability: IBM emphasizes tools for explaining AI decisions and mitigating bias – important for compliance. If you integrate a third-party AI, IBM can layer on monitoring and governance.

Financial-specific solutions: IBM has developed solutions like Cognitive Risk (for compliance analytics), and their IBM Cloud for Financial Services is designed to meet regulatory requirements out of the box (e.g., encryption, data locality). IBM’s legacy in the industry means many existing core systems are IBM-based, so Watson APIs can sometimes integrate more naturally if you’re in that environment. For an SMB, IBM might feel “heavy”, but they do have cloud-hosted APIs like others, and they have a strong consulting arm that can assist in integration (useful if you prefer more hand-holding).

FinTech-Specific Providers: Besides the big general providers, there are niche players focusing on finance AI:

Upstart: As discussed, provides an AI lending API for credit decisions. An SMB bank partnering with Upstart can essentially outsource a chunk of their underwriting to an AI (while still controlling policy).

Feedzai: Offers an AI platform for fraud prevention (especially in payments and merchant risk) – their APIs can integrate into transaction streams to score for fraud in real time.

Featurespace: Known for ARIC (Adaptive Real-Time Intelligence Platform) focusing on fraud/AML anomaly detection. Often used by banks to catch money laundering patterns.

Zest AI: Provides credit model building (they can create custom credit risk models for a lender) with an emphasis on explainability and fairness.

FICO: The traditional scoring company now offers AI tools and has the FICO Falcon Fraud platform (widely used in card fraud detection) which can integrate with banking systems.

Plaid + AI partners: Plaid, famous for connecting bank accounts in fintech apps, isn’t an AI provider per se, but many fintechs use Plaid to get data and then plug into AI services. Some newer companies layer AI on financial account data for insights (for instance, Codat and Yodlee provide transaction data APIs; startups then use AI on that data to offer spending insights or cashflow forecasts).

Insurtech/Fintech crossovers: e.g., Lemonade’s open-source AI or things like Einstein AI by Salesforce (if you use Salesforce CRM in wealth management, Einstein can predict client needs).

These specialized providers can sometimes offer faster deployment for that specific use case because their whole product is tailored to it. The trade-off is they might be narrower in scope than a general cloud provider’s AI. For an SMB, the decision could be: do I go with a big provider’s general tool (which might be cheaper or more integrated with my stack) or a specialist that deeply knows finance? Often, a mix is used – e.g., using a general provider for chatbot, but a specialist for fraud.

4. Best Practices for Seamless AI API Integration

Implementing AI via API requires a mix of technical integration and organizational readiness. Here are some best practices to ensure a smooth journey:

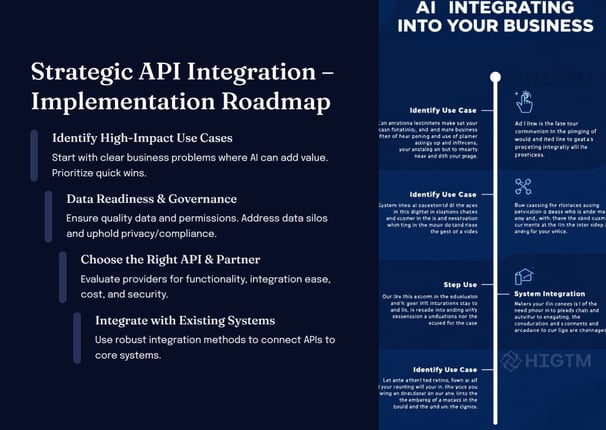

4.1 Start with a Clear Use Case and ROI Expectation

Don’t integrate AI for the sake of saying you did. Identify a pain point or opportunity with measurable metrics. For instance, “We spend 200 hours a month on manual compliance checks – we want to cut that by 50%” or “Our fraud losses are $X, let’s reduce them by 30% within a year using AI.” Clear goals help in choosing the right solution and in later evaluating success.

4.2 Engage Stakeholders Early

Integration touches multiple teams – IT, compliance, business units, customer service, etc. Bring them in early. If you’re adding an AI credit scoring API, involve the credit risk officers and underwriters so they understand and trust the tool. If it’s a chatbot, get input from your call center reps or branch staff for the questions they get often. Early buy-in prevents the “this was thrown at us by IT” syndrome and surfaces practical insights (like what to do if the AI gives an odd result).

4.3 Ensure Data Quality and Access

AI is data-hungry. Audit your data sources – are they accurate, up-to-date, and accessible via an API or batch process? You might need to clean data or even set up new data pipelines to feed the AI. For example, if implementing fraud detection, consolidate transaction logs from all channels into one stream the AI can analyze. Consider using a data warehouse or integration layer to funnel data to the AI API. Also address data permissions – check with legal if customer data can be sent to a third-party AI (often it’s fine if under contract, but things like account numbers or personal identifiers might need hashing or tokenization).

4.4 Prioritize Security & Compliance

We touched on this in challenges – but concretely, work with your cybersecurity team to do a risk assessment of the API integration. Use encryption (TLS) for any data in transit to the API. Consider what data is being returned as well – e.g., if the AI sends back a recommendation, how is that logged? Perform vendor due diligence: ensure the AI provider has necessary certifications (ISO 27001, SOC 2, etc.), and maybe get contractual assurances on data usage (many AI APIs will not use your data beyond serving you, especially if you pay for enterprise service). If you operate in a regulated space (most finance is), document how the AI is being used and how you control it – you’ll need this for audits.

4.5 Use API Management and Modular Architecture

Technically, treat the AI service as a module in your architecture. Use an API management tool or gateway to manage calls, handle retries, and log usage. This also makes it easier to switch providers if needed, since your internal systems would talk to the gateway which then calls the AI API – you can reroute those calls later. Embrace a microservice mindset; e.g., have a microservice for “fraud scoring” that calls the external API. That way, if you ever build your own model or change vendors, the rest of your system doesn’t change – it still calls the “fraud scoring service.”

4.6 Test Extensively (Both Functionality and Bias)

Before fully deploying, test the integration end-to-end. Does the AI API respond within required timeframes? Does it handle peak loads (maybe simulate a day’s worth of API calls in a few minutes to see if any rate limits hit)? Are the results accurate and sensical? In finance, also test for biases or edge cases: e.g., does the chatbot understand a range of customer accents or slang if voice-enabled? Does the credit model treat all demographic groups fairly? It’s crucial to catch any unintended discriminatory patterns early – this might involve having diverse test data or using bias detection tools. Some providers (like IBM) have AI fairness toolkits.

4.7 Plan for Human Override and Continuous Monitoring

No AI is 100% perfect. Design your processes such that when the AI flags something or makes a decision, there’s a way for a human to review or override if necessary. For example, if an AI denies a loan application, perhaps it’s sent to a loan officer for a second look if the customer appeals. Or if the AI chatbot can’t understand a query, it should seamlessly hand off to a human agent. Monitor the performance of the AI regularly. Create dashboards that track key metrics (fraud detection precision/recall, chatbot containment rate, average response time, etc.). Also monitor costs – keep an eye on API usage and make sure it aligns with the budget (sometimes enthusiastic adoption can lead to higher call volumes than anticipated).

4.8 Keep the Bridge Open – Communication is Key

This is more organizational – maintain a strong feedback loop between the executive sponsors and the technical team. For instance, weekly check-ins during the pilot where data scientists/engineers present progress in business terms (“We processed 10,000 transactions with the AI and caught 3 additional fraud cases worth $50k that we would’ve missed, but we also had 2 false alarms we’re tweaking”). Likewise, have business teams share qualitative feedback (“The customers seem to like the chatbot, but it fails when asked about X, so we need to address that.”). This ensures the project stays aligned with business value and that issues are addressed collaboratively. It’s exactly in line with HIGTM’s philosophy of bridging perspectives – neither side should be working in a vacuum.

4.9 Educate and Train End Users

When you introduce AI-driven changes, provide training or at least documentation. If analysts will now see AI-generated risk scores on their dashboard, explain what it is, how to interpret it, and how it should factor into their decisions. If branch staff are getting an AI assistant to help answer customer questions, train them on its capabilities and limitations. By making users comfortable with the new tool, you increase adoption and get better results. Often, one-on-one sessions or workshops can turn skeptics into advocates as they see the AI make their job easier.

4.10 Start Small but Plan for Scale

Begin with a pilot in a controlled scope (one branch, one product line, one internal process) to iron out kinks. But always plan your architecture and strategy with eventual scale in mind. If the pilot succeeds, how will you roll it out to all branches or all customers? Is your infrastructure ready to handle 100x the API calls? It’s easier to design scalable integration from the get-go than to refactor later. Cloud-based APIs do scale on their end, but your systems and workflows need to be prepared to accommodate broader use. Also, think about multi-AI strategy: you might start with one use case, but soon you could have several (fraud, chatbot, etc.). Coordinate these under an overall AI integration roadmap so they don’t become siloed projects that duplicate work or compete for resources.

5. Success Stories: How Industry Players are Thriving with AI APIs

To illustrate these principles, let’s look at a couple of brief examples of AI API integration in action:

Morgan Stanley Wealth Management – Advisor Assist (GPT-4 Integration): In 2023, Morgan Stanley made headlines by leveraging OpenAI’s GPT-4 via API to assist their financial advisors. The challenge was that advisors had to sift through a huge library of research and product information to answer client questions. By integrating GPT-4, Morgan Stanley built an internal tool where an advisor can query in plain English – “What are the key risks of investing in emerging market bonds right now?” – and the AI will retrieve and summarize the firm’s relevant research materials to answer that question. The integration was done carefully: the AI was only fed internal, approved content (to avoid any hallucinations or use of incorrect info), and every answer cites the sources so the advisor can verify. Early reports show it saved advisors significant time and helped them provide prompt, informed answers, which is a competitive advantage in client service. This use case highlights how even highly specialized knowledge work can be augmented with an AI API when integrated well.

Small Commercial Bank – Loan Processing with AI API: Consider a hypothetical (composite) example drawn from several real cases: a regional bank with $5B in assets wanted to streamline its small business loan processing. Traditionally, it took 2-3 weeks to collect documents, review financial statements, run credit scores, and make a decision.

By integrating a suite of AI APIs, they transformed this process:

They used an OCR API (Optical Character Recognition) to extract data from tax returns and financial statements submitted by borrowers (no more manual data entry).

They fed this data into a custom credit risk model they developed using a cloud AutoML service (trained on historical loan outcomes). The model, hosted on the cloud, is invoked via API to get a risk score for each application.

For parts of underwriting that required verification (like ensuring a business was legitimate), they used an external data API combined with AI – for instance, an AI that scans online records or databases for red flags about the business.

They also integrated an e-signature and document analysis API to check the signed application package for completeness (AI can flag if a certain form is missing or if a field is inconsistent).

Throughout, a workflow system orchestrates these API calls and presents the loan officer with a dashboard: key ratios auto-calculated, a risk score with explanation (“Cash flow coverage below threshold, high industry risk”), and any flagged anomalies. The loan officer then focuses on the nuanced judgment calls and relationship aspects, rather than crunching numbers.

The result: loan decisions in 2-3 days instead of weeks. The bank saw a boost in customer satisfaction (business owners got needed capital faster) and was able to handle a higher volume of loans with the same staff. By being an early adopter of such AI integrations, this regional bank started competing (in terms of service speed) with fintech lenders that prided themselves on quick turnaround. In fact, this bank began to advertise “Apply in 10 minutes, get a decision within 48 hours,” which attracted more borrowers. It’s a classic case of using AI to punch above one’s weight in a competitive market.

Mid-Tier Insurance Firm – Fraud and Customer Service Bots: While focusing on banking, it’s worth noting a quick insurance example (insurance is a financial service, and often parallels banking needs). A mid-sized insurance company integrated AI via APIs to handle claims. They used an image recognition API to assess car damage from photos (customers upload accident photos, the AI estimates repair costs). They also deployed a claims chatbot via API that walks customers through filing a claim step-by-step with natural language, integrated into their app. On the back-end, a fraud detection API flags suspicious claims (for example, an AI that matches a new claim’s details with patterns of known fraudulent rings). This combination cut down their claim processing time by 40% and reduced suspected fraud cases, saving millions. The same approach can apply to a bank’s auto loan department or any place you process images or forms – the tools often cross industries.

These stories underscore a common theme: organizations didn’t create AI in a vacuum; they plugged AI into real workflows. The tech is impressive, but it was the integration – connecting AI to existing data, systems, and people – that delivered the result.

6. Conclusion: Seize the AI Advantage with Strategic Integration

The financial industry is in the midst of an AI-driven transformation. What was once the domain of tech giants and multinational banks is now accessible to small and mid-sized players through API integrations. Whether it’s a credit union deploying a smart chatbot to serve customers around the clock, or a payment startup using AI to sniff out fraud, the playing field is leveling out. SMBs in finance have a golden opportunity to leverage these tools to innovate rapidly – improving efficiency, delighting customers, and opening new revenue opportunities – without the heavy lifting of building AI from scratch.

To recap, we discussed how AI APIs can bolster fraud detection, automate tedious financial processes, deliver personalization at scale, engage customers via chatbots, and sharpen risk analysis. We also reviewed the major providers offering these AI building blocks and how to choose and implement them wisely. The journey involves technical integration and cultural adaptation, but with a clear strategy, even challenges like data privacy, legacy systems, and model governance can be managed.

As decision-makers, the imperative is clear: embrace AI thoughtfully, but boldly. The cost of waiting is rising – competitors will gain ground by becoming more efficient and insightful. A report by Betterment forecasts that financial institutions’ spending on AI will more than double between 2023 and 2027, topping $400 billion. Those investments correspond to expectations of massive savings and growth (up to $1 trillion in savings by 2030 in banking, by some estimates). In other words, the gap between adopters and laggards will widen significantly in the next few years.

The silver lining is that adopting AI via APIs is not an all-or-nothing play. You can start with a slice of your operations and expand. But the key is to start – deliberately and soon. And you don’t have to navigate this alone. At HIGTM, we specialize in crafting AI integration strategies for financial SMBs, ensuring that technical possibilities translate into business realities. Our ethos of bridging the gap between data scientists and executives means we help your tech teams and leaders speak the same language, align on goals, and execute effectively.

Innovation, efficiency, competitive advantage – these are the promises of AI integration in finance. With the right approach, SMBs can achieve all three. The technology is ready, the use cases are proven, and the roadmaps are emerging. It’s up to forward-thinking financial leaders to take the wheel.

Is your organization ready to leverage AI APIs for a smarter, faster, more customer-centric finance operation?

Now is the time to act. Start with a clear vision, partner with the right providers (and advisors), and begin the journey. Those who do will not only streamline their present but also future-proof their business in an increasingly digital financial landscape.

Contact HIGTM for a consultation on integrating AI into your finance systems – and let’s write the next chapter of your innovation story together. The competitive edge of tomorrow will belong to those who build it today.

Turn AI into ROI — Win Faster with HIGTM.

Consult with us to discuss how to manage and grow your business operations with AI.

© 2025 HIGTM. All rights reserved.